Wondering what credit score you need to make your dream of owning a home a reality? Confused about what factors lenders consider when evaluating your mortgage application? If yes, look no further! Read this article to know the credit score you need to buy your dream house.

Discover how your credit score determines your ability to buy a house and secure a low mortgage interest rate.

If you have a good credit score, your chances of receiving a mortgage increase. Understand the importance of a good credit score for home loan approval and learn how to improve your credit score if necessary.

Grab all the gist in this article.

To Know What Credit Score You Need to Buy a House, Understand:

1. What Is a Credit Score in General?

2. What Are Good vs Bad Credit Scores?

3. What Is a Good Credit Score to Buy a house?

4. What Is the Minimum Credit Score to Buy a House(By Loan Type)?

5. How to Improve Your Credit Score?

6. What Are the Criteria Mortgage Lenders Look For When Approving a Home Loan?

7. How Can You Buy a House With Bad Credit Score?

Let’s go!

1. What Is a Credit Score in General?

To determine the credit score to get a mortgage, understand what a credit score is.

A credit score is a numerical representation of your creditworthiness, calculated based on your credit history and financial behavior. A credit score helps lenders evaluate your credit risk and make informed decisions about loan approvals and interest rates. Keep in mind that financial institutions, lenders and landlords, among others, use your credit score to evaluate the risk of lending you money.

2. What Are Good vs Bad Credit Scores?

To know which credit score you need to buy a house, know the differences between good vs bad credit scores.

A good credit score reveals your level of financial responsibility, while a bad credit score signals a higher risk of defaulting on loans, credit cards and other debts.

Evaluate your credit history to determine whether you have a good or bad score. Keep in mind that a good credit score opens doors to better loan and credit offers, while a bad credit score can limit your options and result in higher interest rates. Take control of your credit by frequently checking your score and making smart financial choices.

>>>MORE: How to Know My Credit Score

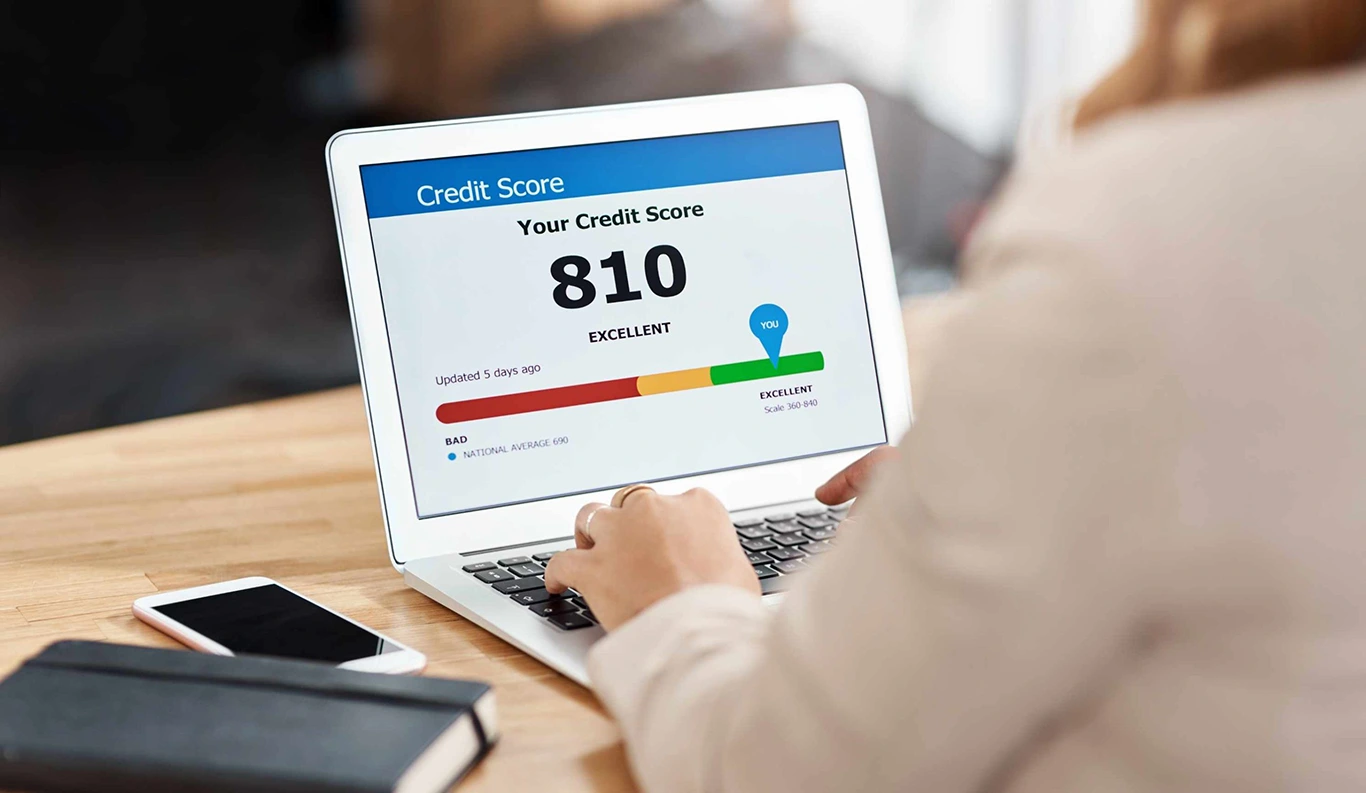

3. What Is a Good Credit Score to Buy a House?

Discover the ideal credit score required to get a home loan and make the process of buying a house seamless.

Bear in mind that depending on the type of loan, a good credit score for purchasing a house varies. To obtain a conventional loan, you need minimum credit score of 620, while some lenders require a credit score of 660 minimum.

Details about credit scores:

• 781 to 850 – Excellent

• 661 to 780 – Good

• 601 to 660 – Fair

• 500 to 600 – Poor

• 300 to 499 – Very poor

4. What Is the Minimum Credit Score to Buy a House(By Loan Type)?

To know which credit score to buy a house, understand the minimum credit score required to buy a house(by loan type).

Understand your credit score – a numerical representation of your creditworthiness that ranges from 300 to 850. The higher your score, the more likely lenders will approve your loan requests. Keep in mind that the credit score standards for conventional and government-guaranteed loans vary.

Conventional Loan Requirements

Make sure you have a FICO score of 620+ before applying for a conventional mortgage. Ensure your credit score remains above 620 to avoid unfavorable loan terms. This way, you improve your chances of approval for a conventional mortgage with lower interest rate. Keep in mind that a government program doesn’t support or guarantee conventional loans. To get a conventional loan approval, submit the following:

- Your mortgage application

- Your documents

- Your credit history

- Your current credit score

Jumbo Loan Requirements

A jumbo loan is a mortgage loan that exceeds the limits set by the Federal Housing Finance Agency for a conventional loan. With Jumbo loans, expect to meet higher credit score and larger down payment requirements compared to conventional loans.

To qualify for a jumbo loan, your lenders want you to have a credit score of 700 or higher. To approve jumbo loan your lenders require you have strong credit ratings and solid financial background. If your FICO score is higher than 740, you have a better chance of obtaining the best jumbo mortgage rates.

Jumbo loans:

- Require a down payment of between 5% and 25% depending on credit and income

- Require higher credit scores

- Are not government-backed

FHA Loan Requirements

To be eligible for an FHA loan, you must have a minimum credit score of 500. Additionally, you’ll need to provide proof of employment, income and a down payment of at least 3.5% of the purchase price of the home.

To secure an FHA loan, you’ll need to pay mortgage insurance premiums, which protects the lender in case you default on your loan. However, if you want to get a better FHA mortgage rate, having a higher credit score can still be helpful.

USDA Loan Requirements

To be qualify for a USDA loan, you must meet certain requirements. You must prove that you are within the income limits set by the USDA, which vary depending on the area you live in. You must be a U.S. citizen, a non-citizen national, or have an eligible immigration status. For USDA loans, most lenders want a credit score of 640 or above. USDA loans:

- Used only for non-urban home purchases

- Require no down payment requirements

- Require a credit score of 640 or higher

>>>PRO TIPS: ChexSystems Security Freeze: How to Properly Do It

5. How to Improve Your Credit Score?

To know which credit score to buy a house, know how to improve your credit score.

If your credit score isn’t high enough to allow you to get a loan but you need one, you can take concrete efforts to improve it. To improve your credit score, consider the following:

- Pay your bills on time and in full every time. Try to pay more than the required minimum each month.

- Maintain your debt repayment schedule, only use available credit when absolutely necessary, and whenever you can, lower your credit limits.

- Spend less than your credit limit.

- Aim to keep your debt payments under one-third of your gross income.

- Avoid using your credit card for cash advances

- Limit new credit applications.

6. What Are the Criteria Mortgage Lenders Look For When Approving a Home Loan?

To know which credit score you need to buy a house, understand what mortgage creditors look for when approving a loan.

Your borrowers analyze your credit history and take into account your present credit outlook when you apply to get a mortgage loan. Your lenders consider the following:

- How long–and varied–is your credit history?

- How is your present debt distributed and what does it look like?

- Have you recently been attempting to access new credit sources?

- How reliable are you in meeting your responsibilities and payments on time?

>>>GET SMARTER: Why Does My Credit Score Go Down?

7. How Can You Buy a House With Bad Credit Score?

To know which credit score you should have when trying to purchase a house, understand how to buy a house with bad credit.

Don’t let a bad credit score stop you from realizing your dream of homeownership. Always keep in mind that each lender has different credit standards. Shop around with other lenders to find a lender who can cooperate with you.

First-time homebuyers can purchase a property in the following methods even with poor or no credit:

- Get a Co-signer

- Improve Your Credit Score by Making a Larger Down Payment

- Ask Different Lenders

Conclusion

To know which credit score to buy a house, know what a credit score is, familiarize yourself with the differences between good and bad credit scores, understand what a good credit score is when buying a house, get familiar with the minimum credit score required to buy a house, and know how to improve your credit score.

That’s not all though; understand what mortgage lenders look for when approving a home loan and finally, know how to buy a house even with a bad credit score.

No Comment! Be the first one.