Our Verdict

If you’re a business owner seeking a financing partner that values a personalized and relationship-oriented approach, KeyBank Business Loans emerges as a dependable option. Boasting a range of loan products, competitive interest rates, and the expertise of seasoned relationship managers, KeyBank positions itself as a comprehensive financial ally.

While the application process may not be the fastest, the bank’s commitment to nurturing lasting partnerships and providing insightful financial advice positions it favourably for businesses looking for more than just transactional interactions.

On the positive side, you stand to gain from the hands-on support of dedicated relationship managers, a diverse array of loan options tailored to meet various needs, and competitive interest rates based on creditworthiness.

However, it’s crucial to note that the potentially lengthier approval process and stringent eligibility criteria might not align with you if you need urgent funding requirements or start-ups grappling with limited credit history. Nevertheless, for if your businesses place value on the depth of a long-term relationship and seek guidance extending beyond mere loan transactions, KeyBank Business Loans proves to be a robust and reliable choice in today’s competitive business financing landscape.

KeyBank Headquarters:

KeyBank National Association

127 Public Square, Cleveland, OH 44114,United States

Pros

- Offers Personalized Service that guides you through the loan process.

- Offers a range of business loan products, including term loans, lines of credit, and SBA loans, with flexibility to meet various business needs.

- Provides competitive interest rates based on your creditworthiness.

Cons

- Has a longer application and approval process compared to online-focused lenders.

- Has a stringent eligibility criterion.

- Place much emphasis on traditional banking practices

Who KeyBank Business Loans Is Best For

Consider KeyBank Business Loans as the best suited for you if you:

- Seek a long-term financial partner to support your growth and expansion.

- Have a track record and established financial history.

- Value personalized service and guidance.

- Require various types of financing, including term loans, lines of credit, and SBA loans.

- Prefer in-person interactions and guidance throughout the loan process.

- Seek for loans with Competitive Interest Rates

>>>MORE: KeyBank Loans Review

Who KeyBank Business Loans Isn’t Right For

Opt for other alternatives aside KeyBank business loan if you:

- Manage Start-ups with Limited Credit History

- Require immediate funding.

- Prioritize a fully online application and approval process

- Prefer entirely digital interactions and are averse to in-person meetings

What KeyBank Business Loans Offers

Loan Variety

- Term Loans: KeyBank offers term loans with flexible repayment terms. These loans are suitable for various business needs, including equipment purchases, expansion projects, or working capital.

- Lines of Credit: Businesses can access revolving lines of credit, providing flexibility to manage cash flow, cover short-term expenses, or take advantage of growth opportunities.

- SBA Loans: KeyBank facilitates Small Business Administration (SBA) loans, offering government-backed financing with favourable terms for eligible businesses.

Competitive Interest Rates

KeyBank provides competitive interest rates based on the creditworthiness of the borrower. This helps businesses minimize financing costs and improve overall financial efficiency.

Personalized Service

The cornerstone of KeyBank’s offering is personalized service. Businesses work closely with experienced relationship managers who guide them through the loan process, ensuring a customized approach that aligns with their unique financial goals.

Flexible Repayment Terms

Repayment terms are designed to be flexible, taking into consideration the cash flow patterns and financial needs of the business. This flexibility allows businesses to manage their loan obligations more effectively.

Experienced Relationship Managers

KeyBank’s relationship managers bring a wealth of experience to the table. They work collaboratively with clients to understand their business, industry dynamics, and financial requirements, providing valuable insights throughout the loan process.

Financial Guidance

Beyond loan products, KeyBank offers financial guidance to help businesses make informed decisions. This includes insights into optimizing cash flow, managing debt, and planning for long-term financial stability.

Local Presence

With a network of local branches, KeyBank offers businesses the advantage of a physical presence. This can be beneficial for those who prefer in-person interactions and value a close relationship with their banking partner.

KeyBank Business Loans Details

Loan Types

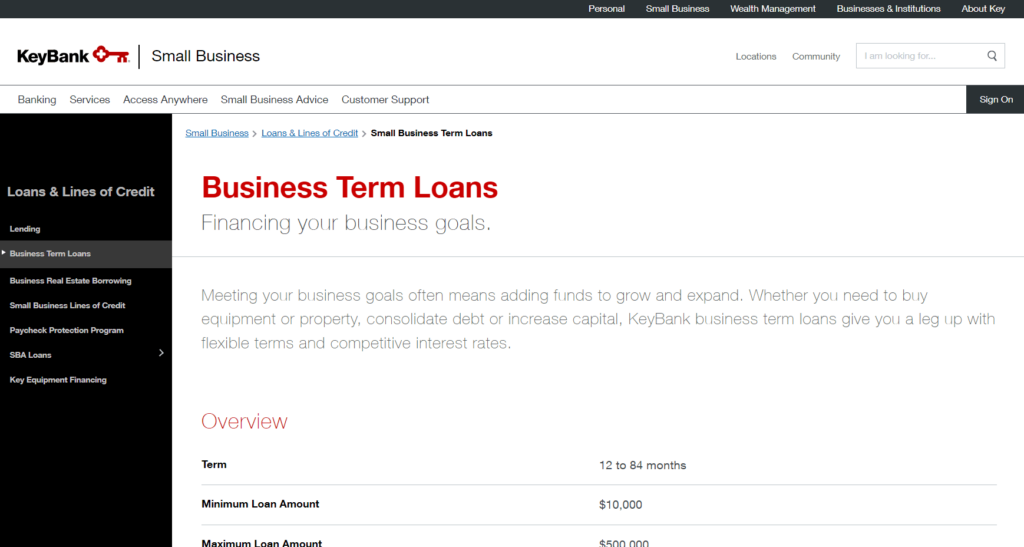

- Term Loans: KeyBank provides term loans that are suitable for various business needs, including equipment purchase, expansion, or working capital. These loans typically have fixed terms and regular monthly payments. Loan Amounts: $10,000 – $500,000. Terms: 1 – 7 years.

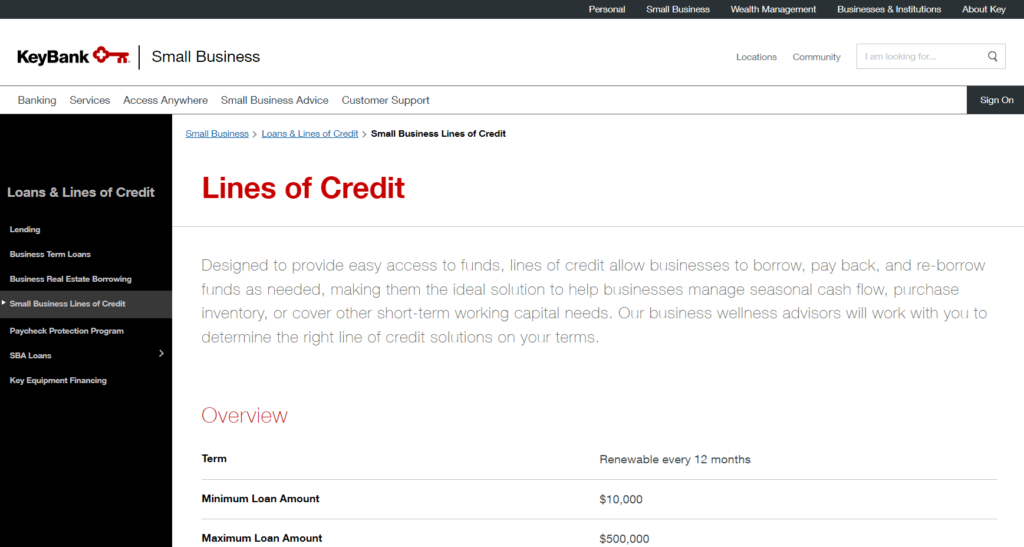

- Lines of Credit: KeyBank offers lines of credit, allowing businesses to access funds on a revolving basis. This flexibility is beneficial for managing short-term cash flow needs, seasonal fluctuations, or unexpected expenses. Loan Amounts: $10,000 – $500,000. Terms: Renewable every 12 months.

- SBA Loans: KeyBank facilitates Small Business Administration (SBA) loans, which are government-backed loans with favourable terms. SBA loans can be particularly advantageous for businesses that meet the eligibility criteria. Loan Amounts: Up to $5 million. Terms: Up to 20 years. Rates: Cannot exceed Prime + 4.75%.

Loan Amounts

The loan amounts offered by KeyBank vary based on the specific needs and financial profile of the business. Businesses can work with KeyBank’s relationship managers to determine the appropriate loan amount for their requirements.

Interest Rates

KeyBank provides competitive interest rates on its business loans. The rates are influenced by the creditworthiness of the borrower and other relevant factors. Businesses with stronger financial profiles may benefit from more favorable interest rates.

Repayment Terms

Repayment terms for KeyBank Business Loans are flexible and can be tailored to align with the cash flow patterns of the business. The terms are typically determined based on the purpose of the loan and the financial capacity of the borrower.

Collateral Requirements

Depending on the type and amount of the loan, KeyBank may require collateral to secure the financing. The specifics of collateral requirements are typically discussed during the application process.

Eligibility Criteria

KeyBank evaluates the eligibility of businesses based on factors such as credit history, financial stability, and the purpose of the loan. Established businesses with a positive financial track record are generally well-suited for KeyBank Business Loans.

Where KeyBank Business Loans Stands Out

Personalized Service

KeyBank is distinguished by its commitment to personalized service. Businesses work with dedicated relationship managers who take the time to understand the unique needs and goals of each client. This personalized approach fosters a strong client-bank relationship.

Diverse Range of Loan Options

KeyBank offers a comprehensive suite of business loans, including term loans, lines of credit, and SBA loans. This diverse range allows businesses to choose the financing option that best aligns with their specific requirements and financial objectives.

Competitive Interest Rates

KeyBank provides competitive interest rates, making it an attractive option for businesses seeking cost-effective financing solutions. The rates are determined based on the creditworthiness of the borrower, allowing financially stable businesses to benefit from favourable terms.

Experienced Relationship Managers

The presence of experienced relationship managers is a standout feature. These professionals bring industry expertise and financial acumen, guiding businesses through the loan application process and providing valuable insights to support informed decision-making.

Local Presence

With a network of local branches, KeyBank establishes a physical presence that is advantageous for businesses preferring in-person interactions. This local touch enhances accessibility and contributes to a more hands-on client experience.

Commitment to Long-Term Relationships

KeyBank places a strong emphasis on building long-term relationships with its clients. This commitment extends beyond individual transactions, creating a partnership that evolves with the changing needs of the business.

Blend of Traditional and Online Services

KeyBank seamlessly blends traditional banking practices with online services. While offering a local, in-person experience, it also provides digital tools for online banking, ensuring a balance that caters to the preferences of a diverse clientele.

>>>PRO TIPS: US Bank Business Loans Review

Where KeyBank Business Loans Falls Short

Application and Approval Time

KeyBank’s application and approval process may take longer compared to online-focused lenders. Businesses in need of quick funding might find the timeline less favourable, especially if they prioritize speed over the benefits of a relationship-driven approach.

Start-ups and Limited Credit History

Startups or businesses with limited credit history may face challenges securing loans from KeyBank. The bank often prefers businesses with a proven track record, which could limit opportunities for newer enterprises.

Emphasis on Traditional Banking

KeyBank’s emphasis on traditional banking practices might not align with businesses that prefer entirely online interactions. Companies seeking a fully digital banking experience might find KeyBank’s model less accommodating.

Potentially Stringent Eligibility Criteria

The eligibility criteria for KeyBank Business Loans may be stringent. Businesses with less-than-perfect credit or those facing financial challenges might find it difficult to qualify for loans from KeyBank.

Limited Small Loan Options

KeyBank may not be the best fit for businesses seeking small, short-term loans. The bank typically focuses on more substantial financing options, and businesses with modest funding needs may find the available choices limited.

How to Qualify for KeyBank Business Loans

To qualify for a KeyBank business loan, you need a minimum of three years in business, and it’s crucial to understand that the bank doesn’t explicitly disclose a minimum credit score or revenue requirement. However, keep in mind that your average net income for the past two years should not exceed $5 million. Remember, when it comes to securing approval, having a higher credit score greatly improves your chances, providing not only access to funds but also more favorable terms and lower interest rates.

Additionally, the specific criteria set by the Small Business Administration (SBA) that you must meet to be eligible are as follows, Your net worth should not exceed $15 million, and your business must operate as a for-profit entity physically located in the US or its territories. It’s essential to meet the SBA’s small business size standards, demonstrate the cash flow capability to handle loan repayments, and confirm that you’re not eligible for or receiving loan funds from other sources. By meeting these criteria, you not only align with KeyBank’s requirements but also adhere to SBA regulations, significantly increasing your chances of a successful loan approval.

How to Acquire KeyBank Business Loans

First, figure out exactly why you need the loan – whether it’s for growing your business, covering everyday expenses, buying equipment, or something else. Next, get to know KeyBank’s rules for eligibility. This includes checking your business’s credit history, how financially stable it is, and how long it’s been running. Make sure your business fits with what KeyBank is looking for.

Now, reach out to KeyBank – give them a call or visit one of their local branches. This is your chance to ask about the types of business loans they have and show them you’re interested in working with them. Set up a meeting with a relationship manager from KeyBank. They’re like your guide through the loan application process. They’ll understand your needs and help you with the application.

Before you apply, get all your paperwork ready – things like financial statements, tax returns, and your business plans. Make sure everything is complete and accurate. Work closely with your relationship manager to fill out the loan application. You’ll be providing important details about your business, why you need the loan, and your financial history. This way, you’re well-prepared for the loan application journey.

Alternatives to KeyBank Business Loans

Funding Circle

Funding Circle is an online lender that specializes in small business loans. It offers a streamlined application process and competitive rates. It’s a good option for businesses looking for quick funding without the traditional banking approach.

OnDeck

OnDeck is known for providing fast and accessible financing to small businesses. It offers short-term loans and lines of credit, making it suitable for businesses with immediate funding needs and less stringent eligibility requirements.

Wells Fargo Small Business Loans

Wells Fargo is a large traditional bank like KeyBank, offering a variety of business loans. Businesses that prefer a traditional banking experience but are exploring options beyond KeyBank might find Wells Fargo’s offerings and branch network advantageous.

Chase Business Loans

Chase is another major bank with a significant presence in business lending. It provides a range of business loan options, including term loans and lines of credit. Businesses already using or considering Chase for their banking needs may find it convenient.

Lendio

Lendio is a loan marketplace that connects businesses with a variety of lenders. It simplifies the process of finding and comparing loan options, making it suitable for businesses seeking a range of financing solutions.

>>>GET SMARTER: Is a KeyBank Personal Loan Worth It?

Customer Reviews

LendingTree outlines the pros and cons, emphasizing a diverse range of SBA lending products, 100% equipment financing availability, and conventional lending options, but cautions about limited SBA product availability and potential transparency issues regarding rates and fees in certain states. ConsumerAffairs® provides consumer reviews and ratings, giving a firsthand account of experiences with KeyBank’s services, including business loans. United Capital Source offers a detailed review covering the advantages, disadvantages, and application process for KeyBank Business Loans.

Pro Tips

- Understand Your Business Needs: Clearly define the purpose of the loan and how it aligns with your business goals. Understanding your needs will help you choose the most appropriate financing option.

- Build a Strong Relationship with Your Relationship Manager: Foster a strong relationship with your KeyBank relationship manager. Effective communication and collaboration will enhance the overall loan experience and provide valuable insights tailored to your business.

- Prepare Your Documentation Thoroughly: Ensure that all required documentation is accurate, complete, and well-organized. A thorough application package can expedite the approval process and demonstrate your business’s financial stability.

- Explore Other Financing Options: While considering KeyBank, explore alternative financing options to ensure you find the best fit for your business. Compare rates, terms, and eligibility criteria to make an informed decision.

Recap

KeyBank Business Loans offers a comprehensive suite of financial solutions with a focus on personalized service and competitive rates. While it may not suit every business type, those valuing a relationship-driven approach will find KeyBank a reliable partner in navigating their financial journey.

No Comment! Be the first one.