Having the bank foreclose on a rental property can create tax implications. You lose rental income but also face tax implications like canceled debt, capital gains, and depreciation recapture. This requires in-depth reporting across multiple IRS forms when filing. Properly accounting for foreclosure of rental real estate takes careful navigation of various tax rules and documentation requirements.

The foreclosure process for you results in canceled debt, transfer of assets, and other financial events that must be reported properly on your tax return to avoid penalties. Having a rental property foreclosed on creates a complicated tax situation.

Consult a tax professional early on for guidance navigating this complex reporting.

- Determine the Tax Implications

- Obtain Form 1099-A from your Lender

- Determine your Tax Basis in the Rental Property

- Calculate the Gain or Loss on the Foreclosure

- Report the Disposition on Form 4797

- Report Any Cancellation of Debt Income

- Report Any Depreciation Recapture

- Complete Form 8582

- Transfer Schedule E Totals to the Appropriate Lines 0n Form 1040

- File the Forms

Recap

1. Determine the Tax Implications

To report a foreclosed rental house on your taxes, recognize the tax implications of a foreclosed rental property. The foreclosure might lead to taxable income or losses depending on various factors, including the property’s fair market value at the time of foreclosure and any outstanding debts forgiven by the lender. Be aware that state and local tax implications may also apply.

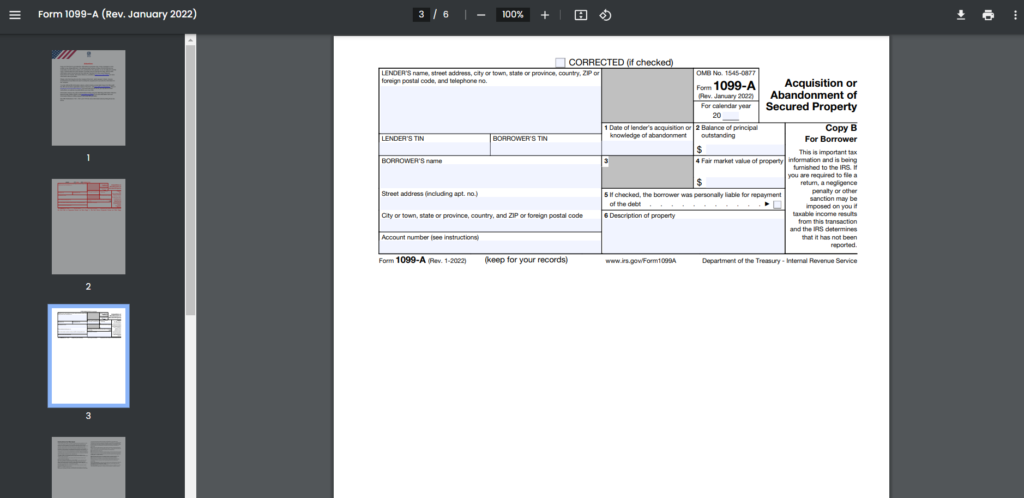

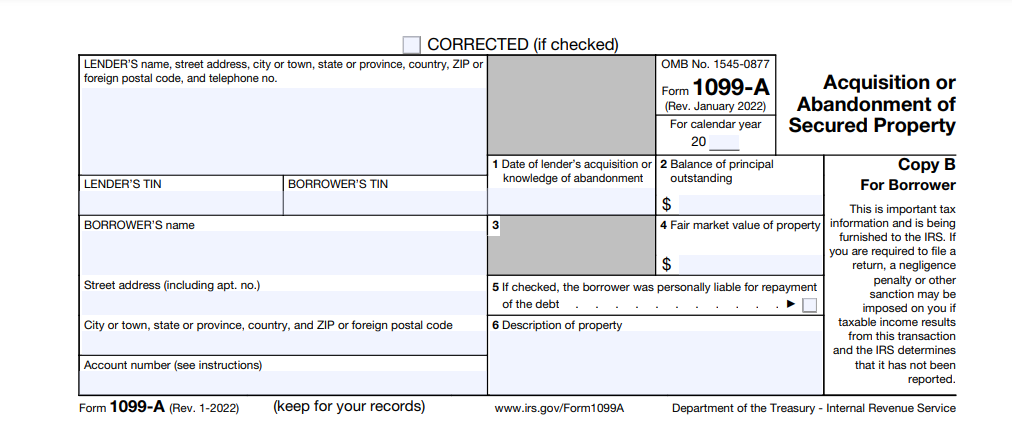

2. Obtain Form 1099-A from your Lender

To report a foreclosed rental house on your taxes, obtain form 1099-A. This will show information like the date of foreclosure, balance owed, and fair market value (FMV).

Form 1099-A is required to be issued by the lender who foreclosed on your rental property. This form provides key details needed to determine the tax implications of the foreclosure.

You should receive a copy by January 31 of the year following the foreclosure. If you do not receive Form 1099-A, contact your lender immediately and request they send it to you. It contains information that must be reported on your tax return.

Obtain this form from the lender and review it for accuracy before filing your taxes. Confirm the date of foreclosure, loan balance, and especially the fair market value (FMV) listed. The FMV may require an appraisal and you can contest the amount if you disagree with their figure.

>>>PRO TIPS: Charitable Contributions: Everything You Must Know

3. Determine your Tax Basis in the Rental Property

To disclose a seized rental home on your tax documents, evaluate your tax basis. This is typically your original purchase price plus improvements made, minus any prior depreciation claimed.

In order to calculate the gain or loss on your rental home foreclosure, you need to know your adjusted tax basis in the property. This serves as your cost figure in the capital gain/loss formula.

Start with the original purchase price paid for the property when first acquired. Then add in the cost of any major capital improvements or additions made over the years like room additions, new roof, electrical, plumbing, etc. Improvements must be capitalized and depreciated.

Next, subtract out all the depreciation expenses you have claimed over the years on the rental property. Depreciation reduces your tax basis each year so this accumulated depreciation must be deducted to arrive at the adjusted basis.

The resulting figure represents your total tax basis amount for the property.

4. Calculate the Gain Or Loss on the Foreclosure

To document a forfeited rental dwelling on your tax forms, calculate the gain or loss. Take the FMV reported on Form 1099-A and subtract your adjusted tax basis.

Now that you have your adjusted tax basis figure, you can calculate the capital gain or loss on the disposition resulting from the foreclosure.

If the FMV is greater than your tax basis, then you have a taxable capital gain on the foreclosure. If your tax basis is higher than the FMV, then you have a capital loss.

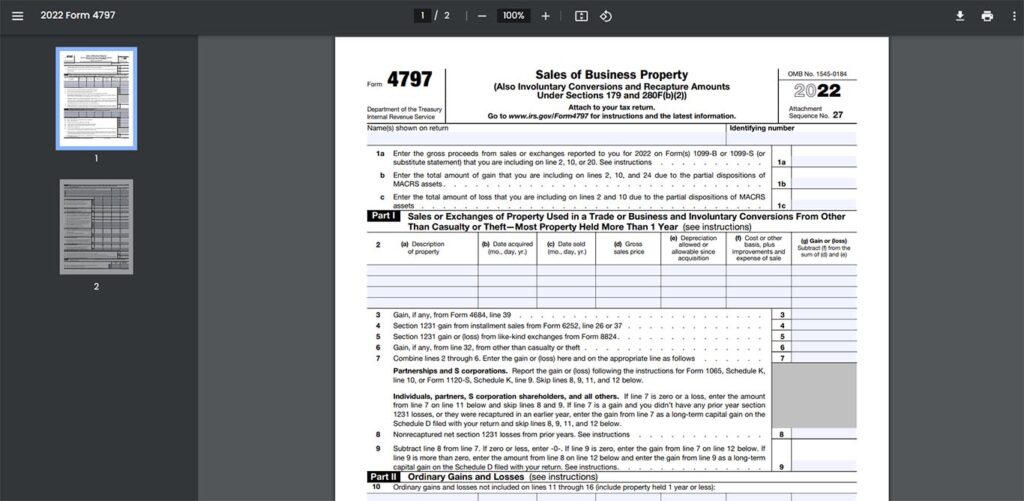

5. Report the Disposition on Form 4797.

To declare a repossessed rental property on your tax return, fill form 4797. This is where you report sales, exchanges or involuntary conversions of business property. Report the FMV proceeds and your tax basis to determine the gain or loss.

The foreclosure of your rental property is treated as an involuntary conversion of business property for tax purposes. That means the transaction must be reported on IRS Form 4797, Sales of Business Property.

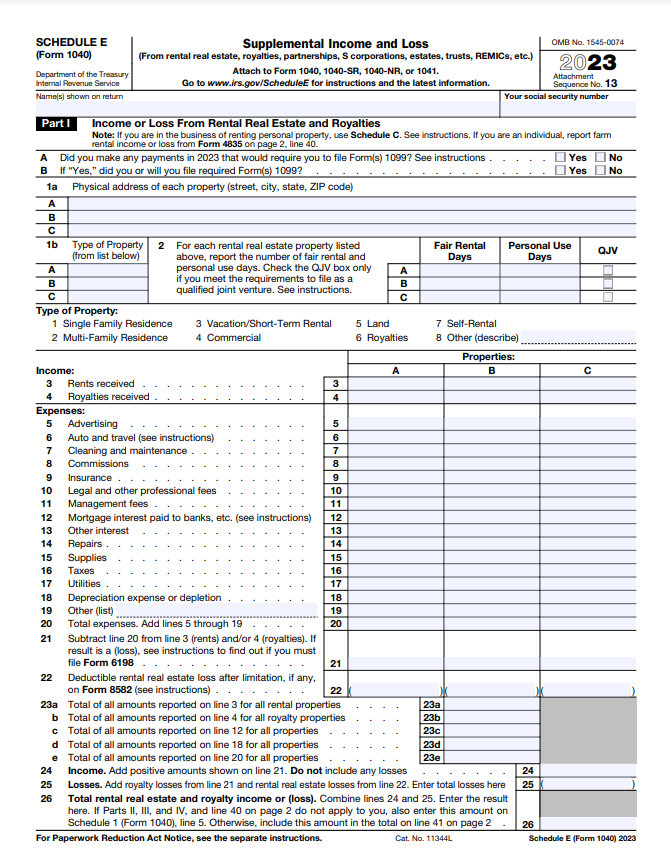

Now that you have accounted for capital vs. ordinary gain/loss treatment, cancellation of debt income, and passive loss limitations, the final deductible amounts must be transferred to your Schedule E.

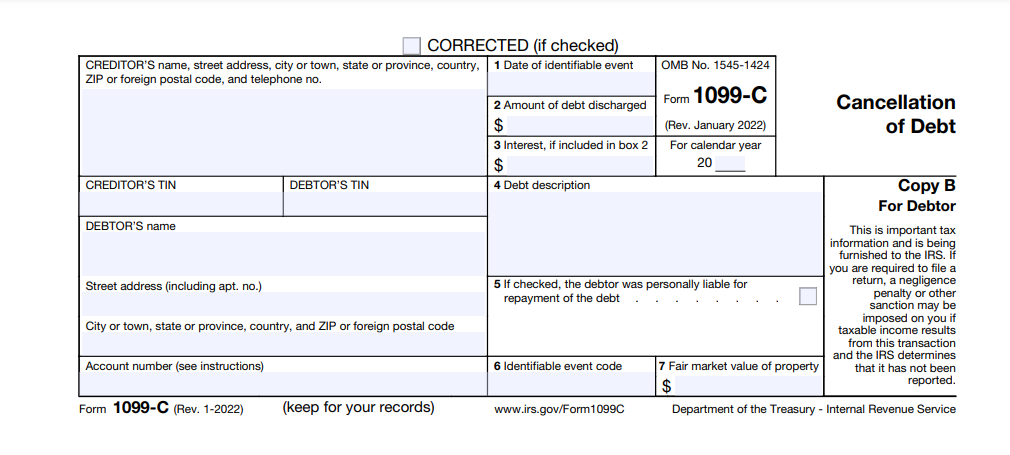

6. Report Any Cancellation of Debt Income

To account for a taken rental house in your tax filings, report any cancellation of debt income. Do this on Form 1099-C separately on Schedule 1 line 8z. You will receive a Form 1099-C if any portion of your rental mortgage was forgiven by the lender.

In addition to the capital gain/loss treatment covered thus far, you may also recognize cancellation of debt (COD) income that needs to be reported if part of your rental property debt was forgiven in the foreclosure.

If the outstanding mortgage loan balance was greater than the FMV provided on Form 1099-A, and the lender cancelled the difference, that amount is treated as taxable COD income.

You will receive Form 1099-C reporting any amount of cancelled debt from the lender. Filing Form 1099-C prevents double taxation.

>>>GET SMARTER: Maximizing Tax Deduction for Business of Your Car

7. Report Any Depreciation Recapture

To log a lost rental property on your tax return, declare any depreciation recapture. If any, do this on Form 4797. This accounts for any excess depreciation claimed over actual decline in FMV.

In addition to capital gain/loss treatment, you also need to check Form 1099-A to determine if there is any depreciation recapture required on the rental property disposition.

If the FMV reported is less than your adjusted tax basis (i.e. a capital loss position), then no recapture applies and you can skip this step.

However, if FMV exceeds your adjusted tax basis (gain position), then some or all of the gain may be treated as depreciation recapture taxable as ordinary income, regardless of holding period.

Any recaptured depreciation flows through to your Schedule E and prevents excess depreciation deductions compared to the property’s true decline in value.

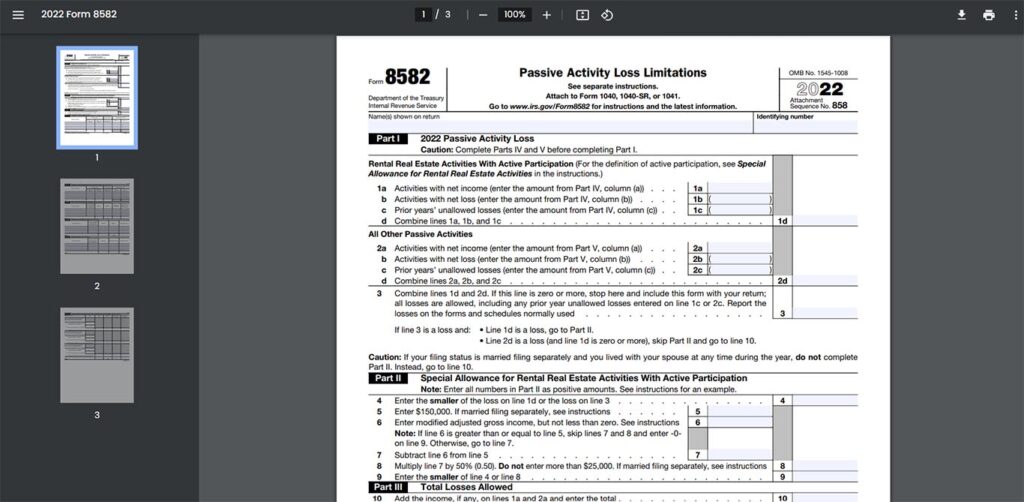

8. Complete Form 8582

To report any passive activity loss limitations that may apply on business or rental losses, fill form 8582.

If your rental property was considered a passive activity, and the foreclosure resulted in a loss, that loss deduction may be limited by the passive loss rules.

Form 8582, passive activity loss limitations, must be completed to determine how much of the loss is currently deductible vs. suspended for future use when offsetting passive income.

Complete form 8582 following the instructions to categorize the loss as passive or non-passive and apply the appropriate limitations.

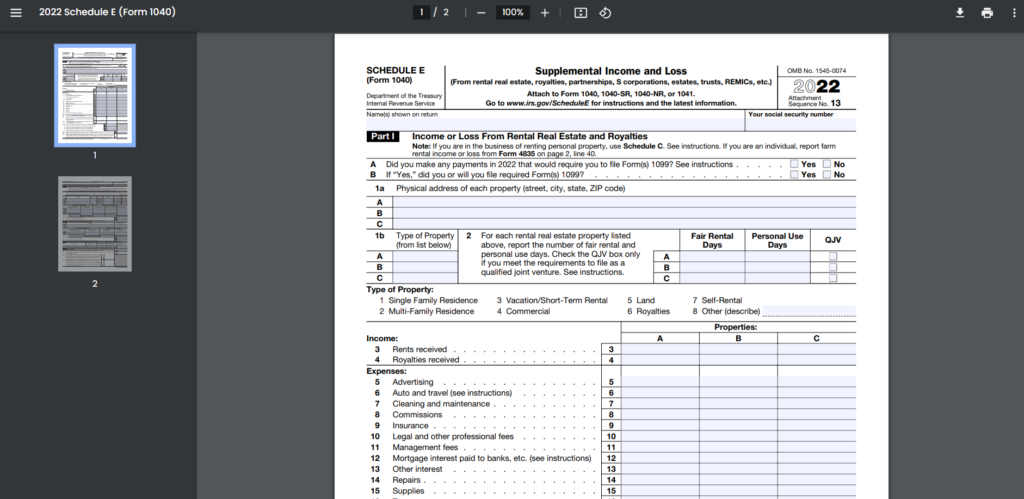

9. Transfer Schedule E Totals to the Appropriate Lines on Form 1040

To itemize a taken rental house in your tax records, transfer Schedule E totals to the appropriate lines on Form 1040. Report rental income on line 17 and any passive loss limitations on line 18.

The final step is carrying over the net amounts from your Schedule E reporting onto your Form 1040 personal tax return.

This brings together all the details of your rental home foreclosure onto your personal 1040 tax return for proper reporting. Consult a tax professional for guidance if needed.

10. File the Forms

To report a foreclosed rental house on your taxes, file form 1099-A, form 4797, form 8582 and schedule E with your form 1040 tax return. As the final step, be sure to include the following forms and schedules when filing your completed Form 1040 tax return:

Form 1099 (A received from lender)

Form 4797 (detailing capital vs. ordinary gain/loss)

Form 8582 (if passive loss rules apply)

Schedule E (reporting net rental income/loss)

File the completed forms with the IRS by the deadline. The deadline for filing tax returns and related forms is typically April 15th unless extended.

Recap

Reporting a foreclosed rental property on your taxes involves several steps – determining basis, classifying gains/losses, limitations on losses, and transfers to the correct forms.

But properly accounting for all tax impacts allows you to maximize deductions and minimize income from the unfortunate foreclosure event. Consult a trusted tax pro if you need assistance navigating this complex reporting process.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult his or her own attorney, business advisor, or tax advisor with respect to matters referenced in this post. . For comprehensive tax, legal or financial advice, always contact a qualified professional in your area. S’witty Kiwi assumes no liability for actions taken in reliance upon the information contained herein.

No Comment! Be the first one.